The 2023 and 2024 hurricane seasons devastated many coastal regions, and we still have a few weeks left of the 2024 season as of the date of this article. As homeowners work tirelessly to rebuild, they face another challenge: a significant number of denied insurance claims. This article explores this alarming trend, examining data from the Florida Office of Insurance Regulation (FLOIR) and the reasons behind these denials. We’ll also discuss legal recourse for homeowners in this unfortunate situation.

Florida’s Hurricane Insurance Claim Data

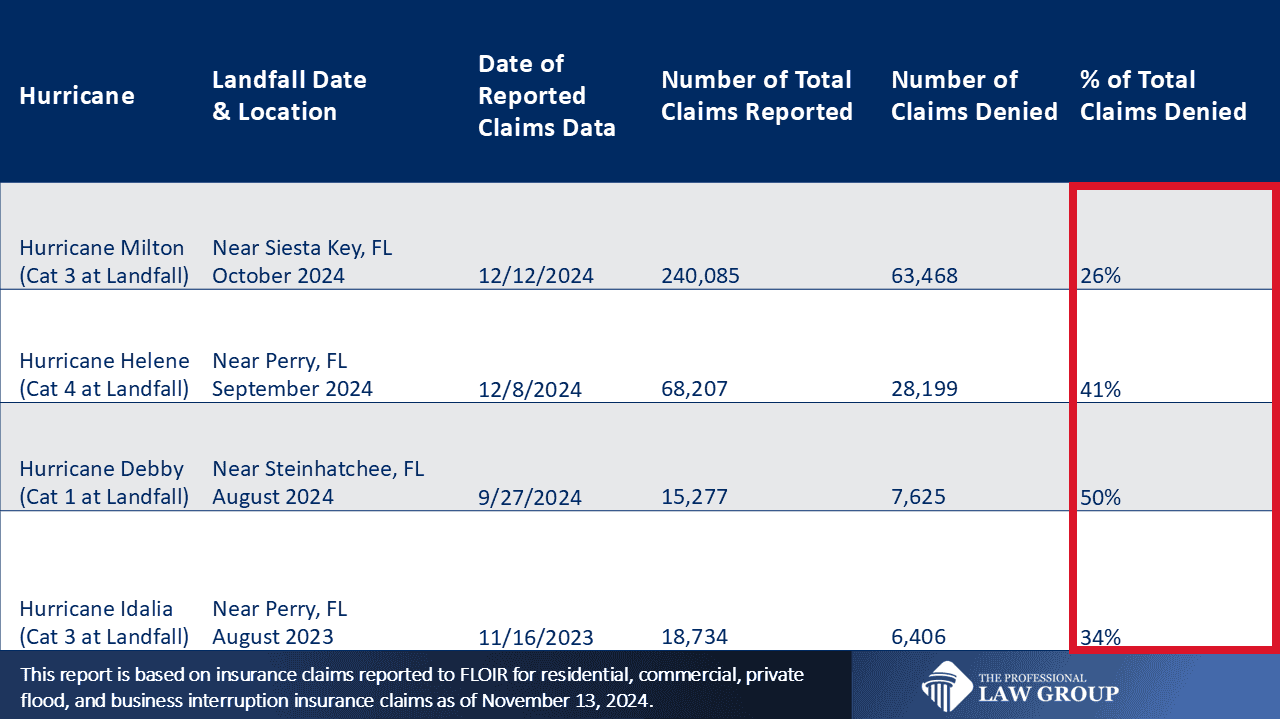

The data we analyzed for this article was collected by the Florida Office of Insurance Regulation (FLOIR) through mandatory data calls. Data calls are required by Florida Statute 624.307 to gather essential information on claims and other relevant details from insurance companies for catastrophic level hurricanes[1].

This article focuses on residential property, commercial property, private flood, and business interruption insurance claims from the mandated data calls for Hurricanes Milton, Helene, Debby, and Idalia[2]. This summary reflects data reported as of November 13, 2024.

Key Findings from the Insurance Claim Data

- Denied claims are prevalent. A concerning trend shows that a substantial portion of insurance claims have been closed without payment by insurance companies, ranging from 26% to 50% depending on the hurricane. This represents denied claims for residential, commercial, private flood, and business interruption claims combined.

- Hurricane Debby has the highest denial rate. While Hurricane Debby was the least intense storm on the list (a Category 1), it had the highest denial rate, with 50% of residential, commercial, private flood, and business interruption claims combined closed without payment.

- Hurricane Milton has the greatest number of claims denied. Hurricane Milton, a Category 3 storm, resulted in the highest number of reported claims (240,085) and the largest number of denied claims (63,468) for residential, commercial, private flood, and business interruption claims combined.

Why Are Insurers Denying Claims?

Several factors are contributing to the surge in denied hurricane claims[3]:

- Underinsurance. Many homeowners may have inadequate coverage to fully address the costs of repairs and replacements.

- Policy exclusions. Hurricane policies often contain specific exclusions, such as those related to flooding or mold damage.

- Appraisal disputes. Disagreements between insurers and homeowners regarding property damage valuation can lead to claim denials.

- Fraud concerns. Unfortunately, fraudulent claims made by property owners can lead to increased scrutiny, sometimes resulting in the denial of legitimate claims.

- Allegations of pre-existing damage. Pre-existing damage is not typically covered by insurance policies. Almost all policies include a clause that excludes pre-existing damage from coverage should the policyholder make a claim.

When to Seek Legal Counsel

Homeowners and commercial property owners and managers who have experienced a denied or underpaid insurance claim should consider seeking legal counsel if:

- The denial lacks a clear explanation.

- The insurance adjuster is unresponsive or unhelpful.

- The insurer offers an unreasonably low settlement.

- There are concerns about fraudulent claim allegations.

An experienced insurance attorney can help navigate the complex claims process, negotiate with insurers, and pursue fair compensation through a lawsuit if necessary. Learn more about Reopening Closed Claims.

Protecting Your Rights in the Wake of a Disaster

As hurricane seasons become increasingly intense, it’s crucial for homeowners to be proactive in protecting their interests. By understanding common reasons for claim denials and knowing when to seek legal assistance, you can increase your chances of a fair settlement and rebuilding your life after a devastating storm.

About The Professional Law Group

We help people and businesses disrupted by property damage from insured events. Through strategic and expert claim management, we aim to recover a fair settlement for our clients to repair damages and get back to normal.

The Professional Law Group serves the entire states of Florida and Texas with offices in Hollywood, FL and Austin, TX. Ready to take the next step? Contact us to schedule a free, no-obligation consultation of your case. Need more information? Meet our creative problem-solving attorneys and staff who work collaboratively every day to provide confidence and leadership to your case from start to finish.

Notes and References

[1] https://www.floir.com/tools-and-data/catastrophe-reporting

[2] FLOIR also reports data for commercial auto and private passenger claims which is not reported in this article.

[3] The Florida Office of Insurance Regulation notes “the most common reasons for a closed claim without payment is not meeting the deductible, or being a claim for flood damage which is not generally covered under a homeowner’s insurance policy. Other reasons include, but are not limited to, the consumer withdrawing the claim or the insured not being reachable to adjudicate the claim. The OIR audits and examines insurer claims payments following every catastrophe to ensure claims are properly handled in compliance with Florida law and the terms of the policy.”